The trend in steel prices was fairly uneven in the third quarter of 2023.

Rising interest rates, persistently high energy prices (even though they have fallen since the crisis in the summer of 2022), the automotive industry, which appears to be stagnating, and the construction industry, which is in decline, are leading to a downward trend in demand for raw materials and therefore for steel.

Furthermore, economic forecasts have been revised downwards in Europe and in most European countries, with Germany even threatening recession. In addition, the fall in activity in China has meant that many Chinese producers have tried to export more at lower prices. These increased imports have not yet been cleared through customs, as the quotas for the third quarter have been used up, but they will be in the fourth quarter, which could further depress steel prices.

Other Asian countries are experiencing the same situation, which is not improving demand for steel in general.

Prices per tonne of steel are therefore falling, to around €850 – €890 per tonne. These are obviously base prices, as there are supplements for different qualities, thicknesses, widths and lengths.

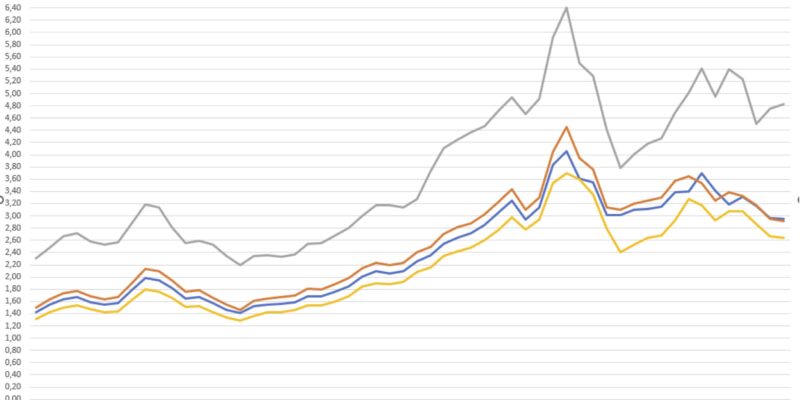

Prices for alloy surcharges for the various categories of stainless steel are also trending slightly downwards. This drop varies according to the quality of the stainless steel.

In view of these factors, it does not seem likely that prices will rise in the fourth quarter. They may stabilise if the stimulus measures taken by certain countries begin to bear fruit.